Government websites often end in .gov or .mil. Before sharing sensitive information, make sure you’re on an official government site.

The https:// ensures that you are connecting to the official website and that any information you provide is encrypted and transmitted securely.

Estimate tax due dates for calendar year filers:

Payment 1 – April 15

Payment 2 – June 15

Payment 3 – September 15

Payment 4 – December 15

Estimate tax due dates for fiscal year filers:

Will be due on the 15th day of the fourth, sixth, ninth, and 12th months of the fiscal year.

The owner of a vessel for which this state is the state of principal use shall deliver to the office an application for a certificate of title for the vessel, with the applicable fee, no later than 20 days after the later of:

Yes, an overpayment from the prior year’s composite return can be transferred to an Electing pass through entity’s account.

No, if the current title is an Alabama ELT there is no cost to print a physical title.

However, once an ELT is printed on physical title paper it can not be printed again. A replacement title application must be applied for if a replacement is needed.

The Alabama taxable income of the Electing Pass-Through Entity will be calculated in accordance with §40-18-24, Code of Ala. 1975, for Partnerships, and §40-18-161 and §40-18-162, Code of Ala. 1975, for S Corporations. Taxable income shall be apportioned in accordance with the provisions of Chapter 27 of Title 40, Code of Ala. 1975. Use the total of total of lines 1 through 17 in the Alabama column on Schedule K, Form 65, or Form 20S, to determine Alabama taxable income. Alabama tax paid under this provision shall not be deducted in calculating Alabama taxable income.

The tax rate is 5 percent.

For tax years beginning on or after January 1, 2021, any Alabama S corporation, as is defined by §40-18-160, Code of Ala. 1975, and any Subchapter K Entity as is defined by §40-18-1, Code of Ala. 1975, may elect to be taxed as an Electing Pass-Through Entity.

An application for a vessel certificate of title must be accompanied by:

A refund may be requested by the entity. To request a refund, use the form PTE-C and list the amount of estimate payments made on line 5b.

The Electing Pass-Through Entity must submit Form PTE-E via My Alabama Taxes at any time during a subsequent tax year or on or before the 15th day of the third month following the close of that tax year for which the entity elects to no longer be taxed as an Electing Pass-Through Entity. Once logged into My Alabama Taxes, the taxpayer will go to the Pass-Through Entity account and click on the Form PTE-E-Update Pass Through Entity Election Status link. The taxpayer will then follow the instructions to revoke the election.

A “homemade vessel” refers to a vessel that was built from scratch by the owner (i.e., I am a carpenter and purchased wood to build my vessel). According to the U.S. Coast Guard, homebuilt vessels are constructed by individuals for their own use and not offered for sale. Because of this, these vessels may not always be built to recreational vessel safety requirements in 46 USC §43 and 33 CFR Subchapter S. The owner should apply for a state assigned HIN from the state issuing authority in the state in which the vessel will be principally operated.

Sale of Homebuilt Vessels. The intention of federal regulations to prohibit the sale of homebuilt recreational vessels that may not meet the safety standards is found within 46 U.S.C. §43 and 33 CFR Subchapter S. However, the Coast Guard recognizes that the sale of homebuilt recreational vessels may be appropriate in limited circumstances.

To allow for the sale of homebuilt recreational vessels, the Coast Guard has determined that the homebuilt recreational vessel must:

An initial Medical Cannabis Privilege tax return is the first return due after the taxpayer is licensed by the Alabama Medical Cannabis Commission. Newly licensed medical cannabis entities (categories of cultivator, processor, dispensary, secure transporter, and testing laboratory, or integrated facility) are required to file an Initial Medical Cannabis Privilege Tax Return (MPT-IN) and to pay the privilege tax reported on the return upon approval of the license but no later than 2 1/2 months after date of licensing or commencement of business in Alabama, whichever occurred first. The MPT-IN is to be filed electronically through the Medical Cannabis Commission’s License portal upon final approval of the medical cannabis license. The MPT-IN filing instructions, including the Medical Cannabis Privilege Tax Calculation worksheet are available at MPT-IN Instructions.

Once your MPT-IN return is processed, a Medical Cannabis Privilege Tax (MPT) account number along with a My Alabama Taxes sign-on ID and access code will be issued. To create a My Alabama Taxes account, the assigned credentials are required. All future MPT returns are required to be submitted electronically through My Alabama Taxes at https://myalabamataxes.alabama.gov/.

Payment of the tax may be made electronically at the time of filing. If payment is to be made by check or money order, it should be submitted with a completed payment voucher (MPT-V) by the payment due date which is 2 1/2 months following the issuance of the license. The MPT-V can be downloaded from the Forms page.

If the Alabama Medical Cannabis Privilege Tax is paid after the payment due date, late payment penalty and interest will be due.

The federal taxable income to be used for S corporations and limited liability entities is the total amount of income passed through to the shareholders, members, or partners. 810-2-8-.01(1)(b) and 810-2-8-.01(1)(c)

If you have received a Medical Cannabis Privilege tax delinquency notice from ALDOR, and you have not filed the required return or made the required payment, do so now to avoid further interest and penalties. Medical Cannabis Privilege Tax Returns must be filed in My Alabama Taxes. See “How do I register for My Alabama Taxes?” if you do not have a My Alabama Taxes account. Instructions can be obtained by clicking on the ALDOR Form page and selecting Medical Cannabis Privilege Tax from the “Categories/Tax” filter. If you are uncertain if a return was required or filed, please forward a copy of the delinquency notice to your tax professional.

Individuals that have a My Alabama Taxes account should complete the following steps:

Individuals that do not have a My Alabama Taxes account and are unable to create one should complete the following steps:

No, Pursuant to §40-18-24 and §40-18-161, Code of Ala. 1975, NOLs are not considered in the calculation of net income.

No, the Electing Pass-Through Entity must submit Form PTE-E via My Alabama Taxes at any time during the tax year or on or before the 15th day of the third month following the close of that tax year for which the entity elects to be taxed as an Electing Pass-Through Entity.

Act 2021-423 does not create a filing obligation for any member of an Electing PTE who would not otherwise have a filing obligation. Note, however, that a member seeking to claim the credit for taxes paid by the Electing PTE will have to file a return and report its distributive share of the income of the entity.

The title application fee is $20 for each application for Alabama certificate of title for a vessel.

Designated Agents shall add the sum of $5 as the commission for each application processed.

License Plate Issuing Officials shall collect an additional $5 as the commission for each application processed. The $5 is deposited in a separate fund maintained by the licensing official to be used in his or her sole discretion for any legal purpose in the operation of his or her office.

As of June 1, 2018, Alabama Act 2018-179 established a formal statewide program, administered through the Alabama State Law Enforcement Agency (ALEA), to address abandoned or derelict vessels (ADVs). There are also non-governmental organizations that are involved with the removal and disposal of ADVs, including the Dog River Clearwater Revival, which has worked with Sea Grant and the NOAA Marine Debris Program to remove vessels from the state’s waterways.

Funding

The Alabama Abandoned and Derelict Vessel Fund, established June 2018 and managed by the Secretary of ALEA, is for payment of the seizure, removal, transportation, preservation, storage, advertisement, appraisal, and disposal of a derelict vessel.

Legislative Overview

Effective June 1, 2018, Act 2018-179, relating to derelict and abandoned vessels, authorizes the removal of a vessel from the waters of this state under certain conditions by a law enforcement officer or a private property owner. Vessels that are found adrift are covered under §35-13-1, Code of Ala. 1975, which states that any person may take up and secure “all property adrift.” In addition, Alabama has laws that make it unlawful to place a “dangerous vessel” in a harbor in the state. Under §33-1-33, Code of Ala. 1975, any owner or agency in control of a vessel that is anchored, moored, or made fast to the shore illegally, or is liable to sink or pollute, or deemed to be derelict, can be charged with a fine if they fail to remove it.

Point of Contact

Please see the link below for additional vessel information:

The Medical Cannabis Privilege tax return due date corresponds to the due date of the entity’s corresponding federal return.

Yes, any Alabama S corporation, as is defined by §40-18-160, Code of Ala. 1975, and any Subchapter K Entity as is defined by §40-18-1, Code of Ala. 1975, may elect to be taxed as an Electing Pass-Through Entity.

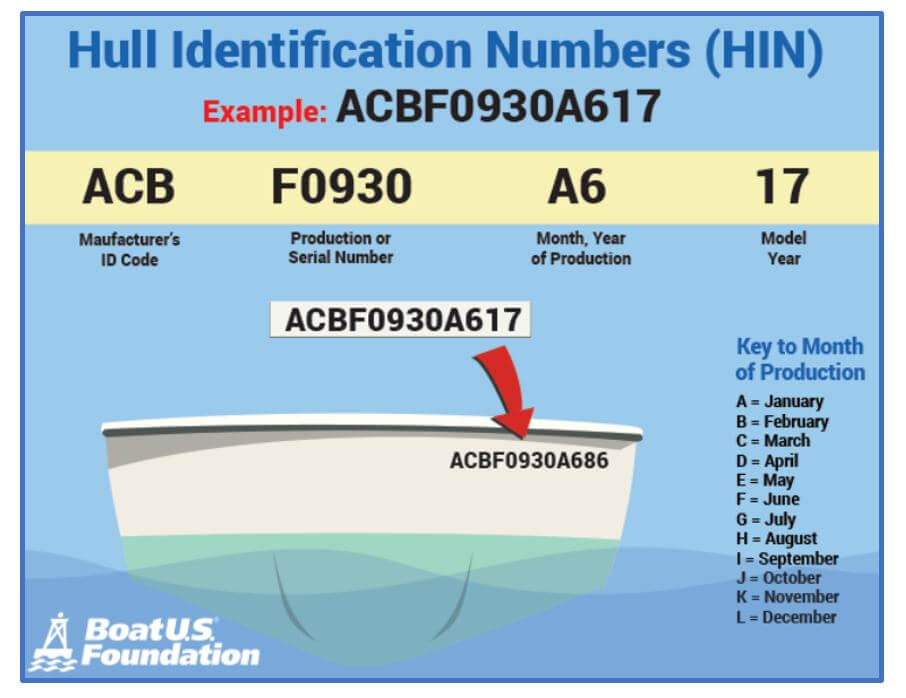

In Alabama, all vessels must have a hull identification number to be registered. If your vessel was manufactured prior to 1972, you would need to apply to the Alabama Law Enforcement Agency’s Marine Patrol (AMP) Division for a State-Assigned Hull Identification Number.

The application needed can be found on the ALEA website at: https://www.alea.gov/sites/default/files/inline-files/HINApplication_0.pdf .

Once this application is submitted to ALEA an officer will contact you to set up an inspection date and time.

A vessel is any watercraft used or capable of being used as a means of transportation on water, except:

A Hull Identification Number (HIN) is the identifying code for a specific vessel. It is a unique combination of letters and/or numbers affixed to the vessel, and is similar to a VIN on a vehicle.

Consist of 12 characters (letters and numbers)

Vessels that meet the following criteria are required to be titled in Alabama:

Prepare and submit the amended return through My Alabama Taxes.

Enter Your Banking Information on the payment page:

Note: If you have debit block on your bank account, please provide the following information to your bank so that your bank will allow the tax payment(s) to be processed without rejecting:

| MAT6045055 | (Company ID #) for Alabama Department of Revenue Payments |

| 2621862182 | for Company ID #’s for Self-Administered Jurisdiction Payments |

Payment Date: Payment Date is the date the payment will be sent to your bank. This date will default to the current date if payment is authorized prior to 4:00 p.m. CST, or the next day if payment is authorized after 4:00 p.m. CST. The Payment Date is editable if your payment is for a current return and is initiated before the Remit Due Date. In this case, you can choose to warehouse your payment up to the Remit Due Date.

If you wish for the payment to not be deducted from your bank account until the due date, you must edit the payment date field and enter that date. You can change this date to any date from the default Payment Date up to the remit due date. Unless you select a later date, the payment will be deducted from your bank account the next business day and paid directly to the government entity(s) listed under Pay To The Order Of.

Due Date: Due Date is the last date in which the payment is due before it is considered delinquent. PLEASE NOTE: To be considered timely paid an EFT payment must be transmitted by 4:00 p.m. CST on or before the Due Date so that the funds are immediately available to the State on the first banking day following the due date of payment.

Remit Due Date: Remit Due Date is the date in which you must submit the return for the EFT payment to be considered timely paid. NOTE: To be considered timely paid an EFT payment must be transmitted by 4:00 p.m. CST on or before the Due Date so that the funds are immediately available to the State on the first banking day following the due date of payment.

Early Filing and Payment, and Warehousing the Payment: If you make your payment prior to the Due Date, the payment will be deducted from your bank account the next business day. However, you can choose to warehouse your payment up to the Remit Due Date so that the payment is not deducted from your bank account until the date you specified.

If you wish for the payment to not be deducted from your bank account until the DUE DATE, you must edit the payment date field and enter that date. You can change this date to any date from the default Payment Date up to the remit due date. Unless you select a later date, the payment will be deducted from your bank account the next business day and paid directly to the government entity(s) listed under Pay To The Order Of.

Late Filing and Payment: If your return and payment are not timely filed and paid, you will be billed the appropriate interest and penalty. You cannot edit the Payment Date field for late payments. The payment will be deducted from your bank account the next business day from the Payment Date.

Pay To The Order Of:

Amount: The payment amount that will be deducted from your bank account.

Click the Continue button to verify the payment. Once verified, click the Authorize button to initiate the payment and receive your confirmation number.

A vessel the ownership of which is recorded in a registry maintained by a country other than the United States which identifies each person that has an ownership interest in a vessel and includes a unique alphanumeric designation for the vessel.

Yes, Electing Pass-Through Entities that have an Alabama income tax liability in excess of $500 must pay estimated tax. An Electing Pass-Through Entity shall be subject to the provisions of §40-18-80.1, Code of Ala. 1975 (estimated tax for corporations). The required installments shall be 25 percent of the required annual payment. Required annual payment generally means the lesser of a) 100 percent of the tax shown on the return for the taxable year, or b) 100 percent of the tax shown on the return of the corporation for the preceding taxable year.

Individual taxpayers needing assistance with the credit claim process or who have questions about available tax credits should call the Individual Income Tax Audit and Appeals Division at 334-353-9770.

The Medical Cannabis Privilege Tax is required to be filed electronically. The initial return (MPT-IN) is to be filed electronically through the Medical Cannabis License Application Portal upon approval and issuance of the Medical Cannabis License. The Annual Medical Cannabis Privilege Tax return (MPT) is required to be filed electronically through ALDOR’s Online filing and payment system – My Alabama Taxes. The Instructions for the MPT-In and Annual MPT filing and MPT Payment Voucher (MPT-V) are available for download (revenue.alabama.gov, click on Forms). Select “Medical Cannabis Privilege Tax” in the “Categories/Tax” drop down box in the Filter Forms search tool.

§20-2A-80(b)(1), Code of Ala. 1975, requires all licensed medical cannabis entities (categories of cultivator, processor, dispensary, secure transporter, and testing laboratory, or integrated facility) to file the Medical Cannabis Privilege Tax Return and to pay the privilege tax.

The federal taxable income to be used for S corporations and limited liability entities is the total amount of income passed through to the shareholders, members, or partners. 810-2-8-.01(1)(b) and 810-2-8-.01(1)(c)

To determine the tax rate for the Medical Cannabis Privilege Tax, begin with the federal taxable income. Then multiply that amount by the taxpayer’s apportionment factor. The resultant amount is used to determine the appropriate rate from the rate schedule.

The pass-through entity must make the election to be treated as an Electing Pass-Through Entity by submitting the Pass Thru Entity Election, Form PTE-E, online via My Alabama Taxes at any time during the tax year or on or before the 15th day of the third month following the close of that tax year for which the entity elects to be taxed as an Electing Pass-Through Entity. Once logged into My Alabama Taxes, go to the Pass-Through Entity account and click on the Form PTE-E-Update Pass Through Entity Election Status link. The taxpayer will then follow the instructions to make the election. The election is binding for that year and all subsequent tax years unless the entity properly elects to no longer be taxed as an Electing Pass-Through Entity. Please note there is no paper equivalent of this online election.

The election shall be accomplished by a vote by or written consent of the members of the governing body of the entity as well as a vote by or written consent of the owners/shareholders holding greater than 50 percent of the voting control of the entity, within the time prescribed above.

The owner, member, partner, or shareholder of an electing pass-through entity shall be entitled to a refundable credit in an amount equal to its pro rata or distributive share of the Alabama income tax paid by the electing pass-through entity with respect to the corresponding tax year.

Estimated tax payments not paid by each quarterly due date will be subject to interest on the underpayment, determined by applying the underpayment rate established by 26 U.S.C. §6621 (as provided by §40-18-80.1, Code of Ala. 1975) to the underpayment for the period of underpayment. In addition, the 10 percent penalty provided for in §40-2A-11, Code of Ala. 1975, applies to estimated tax payments not paid by the quarterly due date.

ALDOR’s titling system, ALVIN, features a VIN decoder that populates this information.

However, there will be occasion where it will not be pre-populated. Sometimes it will populate the information after a vehicle trim is selected.

It is recommended to look up the vehicle year, make, model, and specifications in a Google-type search to see if you are able to find the unladen weight or GVWR.

Another alternative is the NHTSA VIN decoder (https://vpic.nhtsa.dot.gov/decoder/). It will sometimes provide this information for vehicles.

If all else fails and you still can’t determine the unladen weight, then you can enter the same amount as was entered or pre-populated for the GVWR.

The Alabama Law Enforcement Agency’s Marine Patrol (AMP) Division is responsible for issuing a State-Assigned Hull Identification Number or a Replacement Hull Identification Number.

The application needed can be found on the ALEA website at https://www.alea.gov/sites/default/files/inline-files/HINApplication_0.pdf. Once this application is submitted to ALEA, an officer will contact you to set up an inspection date and time.

Yes, Alabama does issue ELTs. If a designated agent (non-licensing official) is set-up for ELT, then any titles issued recording their lien will be issued as an ELT.

The 2017 Alabama Historic Rehabilitation Tax Credit and the Railroad Modernization Act Credit must be claimed at the Electing Pass-Through Entity level and will not be passed through to the partners of the entity.

ALDOR requires the use of Schedule EPT-C, when claiming tax credits. The schedule allows the taxpayer to compute the total amount of tax credits allowable. The amounts entered on the Schedule EPT-C will carry over to the Form EPT, page 1. Many credits now must be claimed on the taxpayer’s My Alabama Taxes account to receive the credit and the Schedule EPT-C attached to Form EPT. For more information on credits, please visit ALDOR’s Tax Incentives page and see instructions for Schedule EPT-C.

The Annual Alabama Medical Cannabis Privilege Tax return is required to be filed electronically through ALDOR’s Online filing and payment system – My Alabama Taxes. There is no paper filing option for this return.

If you are making a payment by check, mail your payment along with Form MPT-V to:

Alabama Department of Revenue

Medical Cannabis Privilege Tax Section

P.O. Box 327320

Montgomery, AL 36132-7320

All credits that require pre-certification must be submitted through My Alabama Taxes. Individual filers can remit the necessary information through their individual income tax account in My Alabama Taxes, or by selecting the “Submit a Credit Claim” option from the “Other links” menu in My Alabama Taxes. The credits that require pre-certification by individual income tax filers are:

*The Neighborhood Infrastructure Incentive Plan Credit – This credit expired in 2015. However, there may be some individual income tax filers that still qualify to claim this credit since there is a 10-year period over which the credit can be claimed.

My Alabama Taxes is ALDOR’s online filing and payment system. All future annual MPT returns are required to be filed electronically through My Alabama Taxes.

Once approved and the Medical Cannabis License is issued, ALDOR will receive the registration information from Alabama Medical Cannabis Commission’s license application. A Medical Cannabis Privilege Tax (MPT) account will be issued to the taxpayer. The account number along with a Sign-On ID and Access Code for My Alabama Taxes will be provided in an “Online Filing Info” letter to the taxpayer. Once this letter is received, taxpayers need to visit https://myalabamataxes.alabama.gov/_/#1. In the upper right side of the screen, you will see Username, Password, and Sign In. Beneath that you will see the link “Create a My Alabama Taxes account.” Click this link to register. Select: Medical Cannabis Privilege Tax. Then provide the Account number, Sign On ID, and Access Code. This information is located on the (Online Filing Info) letter.

Contact the Business Privilege Tax Section (334-242-1170, option 8) if you have questions about the Medical Cannabis Privilege Tax.

The Alabama Department of Revenue’s records indicate the required return and payment for the tax due have not been received. Businesses licensed by the Medical Cannabis Commission are liable for the Alabama Medical Cannabis Privilege tax for each taxable year during which the business is licensed – regardless of the level of business activity. The minimum Medical Cannabis Privilege tax is $100, and the maximum Medical Cannabis Privilege tax is $15,000.

Personal watercraft (PWC) is defined as a type of motorboat which is specifically designed to be operated by a person or persons sitting, standing, or kneeling ON the vessel rather than INSIDE the vessel.

Personal watercraft (PWC) is limited to under 16 feet in length.

The term PWC includes jet skis, wet bikes, etc.

Estimated tax payments made by check should be submitted with the form PTE-V and mailed to the address provided on the form. Please note: §41-1-20, Code of Ala. 1975, requires all single tax payments of $750 or more to be made electronically.

Electronic Payment Options Available:

ACH Debit – My Alabama Taxes – Taxpayers may make electronic payments via My Alabama Taxes for estimate, extension, return and billing payments. A My Alabama Taxes user id is not required to make an electronic payment, but it is recommended.

New taxpayers, who have recently registered with the Alabama Secretary of State, will receive an Online Filing Information letter. The Online Filing Information letter is for “information purposes” and provides the taxpayer with a Sign On ID and Access Code which permits access to My Alabama Taxes.

ACH Credit – Taxpayers making e-payments via ACH Credit must be pre-approved by ALDOR. Log on to My Alabama Taxes and select “Submit an Electronic Funds Transfer Authorization Agreement Form” under Other Actions to submit the form electronically. You must enter a valid business operational reason for using ACH Credit instead of ACH Debit.

No, if an entity elects to be treated as an Electing Pass-Through Entity, the composite return is not required. If an election is not made, partnerships are required to make a composite payment in accordance with §40-18-24.2, Code of Ala. 1975.

A credit card transaction fee is a charge added to the regular price of an item by a retailer when the purchaser pays for the item using a credit card. Other names for this fee include swipe fee, credit card surcharge, processing fee, service charge, or convenience fee.

These fees are subject to sales and use tax and should be included in the seller’s gross sales on retail transactions when calculating tax due. Example: A sale of tangible personal property totals $100. The customer pays with a credit card and is charged a $3 credit card transaction fee. The total price of $103, including the credit card transaction fee, is subject to sales and use taxes.

A credit card fee, even if separately stated, is part of the retailer’s cost of doing business, and the entire consideration for the sale of tangible personal property is subject to sales and use taxes.

If a transaction consists of only non-taxable goods or services, the credit card transaction fee is not subject to sales and use taxes. Example: A customer is charged $50 for a haircut. The customer pays with a credit card and is charged a $3 credit card transaction fee. Since the haircut is not subject to sales and use taxes, the corresponding credit card transaction fee is not subject to sales and use taxes.

Yes, the following documents will be required to be uploaded when filing the return:

A vessel covered by a certificate of documentation issued pursuant to 46 U.S.C. 12105.

The term does not include a foreign-documented vessel.

The Alabama Medical Cannabis Privilege Tax is levied on all persons doing business in Alabama under Title 20 Chapter 2A – the Darren Wesley ‘ATO’ Hall Compassion Act. See Section 20-2A-80(b)(1), Code of Alabama 1975.

Yes, taxable income includes guaranteed payments.

Yes, Alabama allows resident individuals to claim a tax credit for income taxes imposed by other states. This credit is claimed on Form 40, Schedule CR. A copy of the other state’s return and a copy of the state Schedule K-1 should be included as documentation of this credit.

If the individual does not file an individual income tax return in the other state or the state provides an exclusion of income, include a proforma return calculating the tax at the other state’s rate and a copy of the state Schedule K-1 as documentation of this credit.

Note: Any Pass-Through Entity tax deducted on the Pass-Through Entity’s federal return, which reduces the taxable income reported on the owner’s K-1, should be added back to compute Alabama taxable income.

If you have received a Medical Cannabis Privilege tax delinquency notice from the Alabama Department of Revenue, and you have not filed the required return or made the required payment, do so now to avoid further interest and penalties. Medical Cannabis Privilege Tax Returns must be filed in My Alabama Taxes. See “How do I register for My Alabama Taxes?” if you do not have a My Alabama Taxes account. Instructions can be obtained by clicking on the ALDOR Form page and selecting Medical Cannabis Privilege Tax from the “Categories/Tax” filter. If you are uncertain if a return was required or filed, please forward a copy of the delinquency notice to your tax professional.

If the credit is from a Schedule K-1 issued by a pass through entity, the credit claim will be submitted by the pass-through entity, and no action is required by the individual. The credit claim must be submitted by the entity and approved by the Alabama Department of Revenue before the credit will be allowed on an individual’s income tax return. The pre-certification process must be completed by each entity that was allocated a credit until the credit is allocated to the individual claiming the credit. Additional information about credit pre-certification for pass-through entities can be found at https://revenue.alabama.gov/tax-incentives/.

These credits will be subject to an approval process when the tax return is filed claiming the credit. The following are credits that do not require pre-certification by an individual income taxpayer through My Alabama Taxes:

*Alabama Accountability Act Credit – Scholarship Granting Organization (SGO) portion – The process for reserving a donation to an SGO remains unchanged. Only pass-through entity filers are required to complete the new pre-certification process in My Alabama Taxes for donations made to an SGO when the Alabama Accountability Act Credit is passed through to its members.

**Investment Credit (Alabama Jobs Act) – The approval of this credit is managed through the Department of Commerce. Once the Department of Commerce has approved the annual certification, ALDOR will notify the investing company to complete an allocation schedule through My Alabama Taxes. See https://revenue.alabama.gov/tax-incentives/.

***Growing Alabama Credit and Innovating Alabama Credit – The process for reserving a donation to an EDO remains unchanged.

The application for vessel title must be electronically submitted to ALDOR and contain the following:

A “rebuilt vessel” refers to a vessel that is piecemealed together from one or more vessels (i.e., I have the pontoons from a 1992 pontoon boat, I have a frame and floor from a 2005 pontoon boat, and I affix them together to create a “rebuilt vessel”).

ALEA will require a “rebuilt vessel” to meet the same requirements as a Homebuilt Vessel with regard to the future sale of said vessel in order to comply with federal requirements regarding the issuance of a Hull Identification Number (HIN).

The relationship between a taxpayer’s Determination Period and the taxpayer’s taxable year is, at first, confusing. But, to understand how to properly compute the Alabama Medical Cannabis Privilege Tax, one must first understand the terms Determination Period and Taxable Year.

DETERMINATION PERIOD: The determination period is defined in §40-14A-1, Code of Ala. 1975, as “the taxpayer’s taxable year next preceding the taxpayer’s current taxable year.”

Generally, the Determination Period is the taxpayer’s previous taxable year.

TAXABLE YEAR: the taxable year is defined in §40-14A-1, Code of Ala. 1975, as: “the fiscal year used by the taxpayer to file returns required under the income tax levied by Chapter 18 or the financial institution excise tax levied by Chapter 16, or, in the case of an insurance company subject to the premium tax levied by Chapter 4A of Title 27, the calendar year.”

Generally, Taxable Year means the year (whether calendar year or fiscal year) used by the taxpayer to report its taxes.

A vessel inspection by ALEA is to verify that a Hull Identification Number (HIN) does not already exist on the hull.

This inspection is not to determine sea worthiness of a vessel.

The owner of a vessel that is 26 feet or more in length and to which Alabama is the state of principal use on or after January 1, 2024, may voluntarily apply for a certificate of title regardless of when the vessel was constructed.

If you believe you received the delinquency notice in error and have filed the required return, please provide a copy of the return submission confirmation and proof of payment after consulting with your tax professional. Attach copies of the return confirmation and proof of payment to a copy of the Medical Cannabis Privilege tax delinquency notice and email to medicalcannabisprivilegetax@revenue.alabama.gov or mail the response to:

Alabama Department of Revenue

Income Tax Administration

Business Privilege Tax Section – Delinquency Notice Response

P.O. Box 327900

Montgomery, AL 36132-7900

All credits except the 2017 Alabama Historic Rehabilitation Tax Credit and the Railroad Modernization Act Credit shall pass through to and may be claimed by an eligible taxpayer.

The Electing Pass-Through would complete Schedule PC. The amounts entered on the Schedule PC will carry over to the Schedule K and K-1s. Many credits now must be claimed on the taxpayer’s My Alabama Taxes account to receive the credit and the Schedule PC attached to Form 65 or 20S. For more information on credits, please visit ALDOR’s Tax Incentives page and see instructions for Schedule PC.

My Alabama Taxes: Taxpayers can make ACH debit payments and credit card payments through their My Alabama Taxes account.

My Alabama Taxes billing payment: Make an ACH debit payment or credit card payment by clicking Pay A Bill I’ve received under Quick payments from the www.myalabamataxes.alabama.gov home screen. A My Alabama Taxes login is not required, just the billing letter received.

Taxpayer Assistance Group (TAG): Call 334-353-8096 to make a credit card payment over the telephone.

Mail: Check or money orders may be mailed if the amount owed is less than $750. Attach voucher Form MPT-V and payment.

Mail to address below:

Alabama Department of Revenue

Business Privilege Tax Section

P.O. Box 327320

Montgomery, AL 36132-7320

If an extension has been granted for federal purposes, the extension is also granted for Alabama purposes; the Federal Form 7004 must be submitted with the Form 65/20S. The extension only applies to filing a return. No extensions are granted for payment of taxes due.

NOTE: This is an extension for filing purposes ONLY. The full amount of the tax liability is due by the original due date of the return. Payments should be submitted with Form PTE-V Pass Through Income Tax Voucher.

No, an Electing Pass-Through Entity’s taxable income is calculated in accordance with the provisions §40-18-162, Code of Ala. 1975, as appropriate, and apportioned in accordance with the provisions of §40-18-27, Code of Ala. 1975.

Pass-through entities that file an election to be an Electing Pass-Through Entity must file Form EPT, in addition to Form 65 or 20S, and pay the tax due. The pass-through entity’s tax return is due on the 15th day of the third month after the close of the tax year (i.e., March 15 for calendar year filers).

When trying to complete title applications for vessels that have inches listed on the MSO, please use this Vessel Length Chart for conversion purposes.