Individual Income Tax:

General Information for Individuals

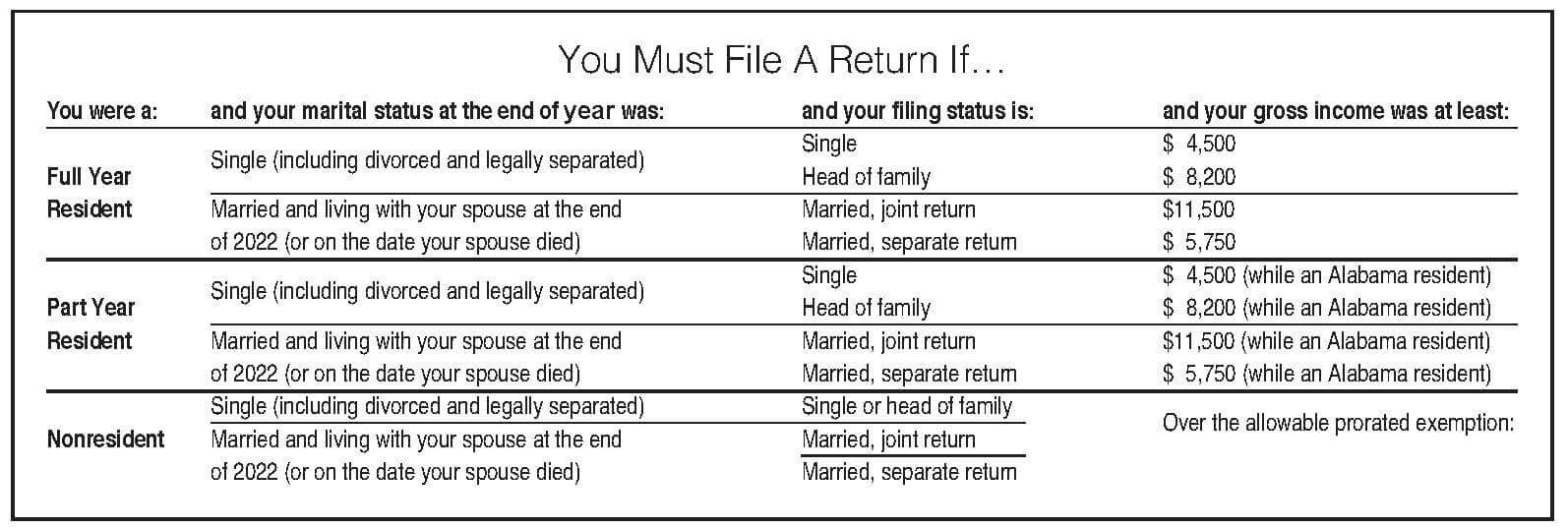

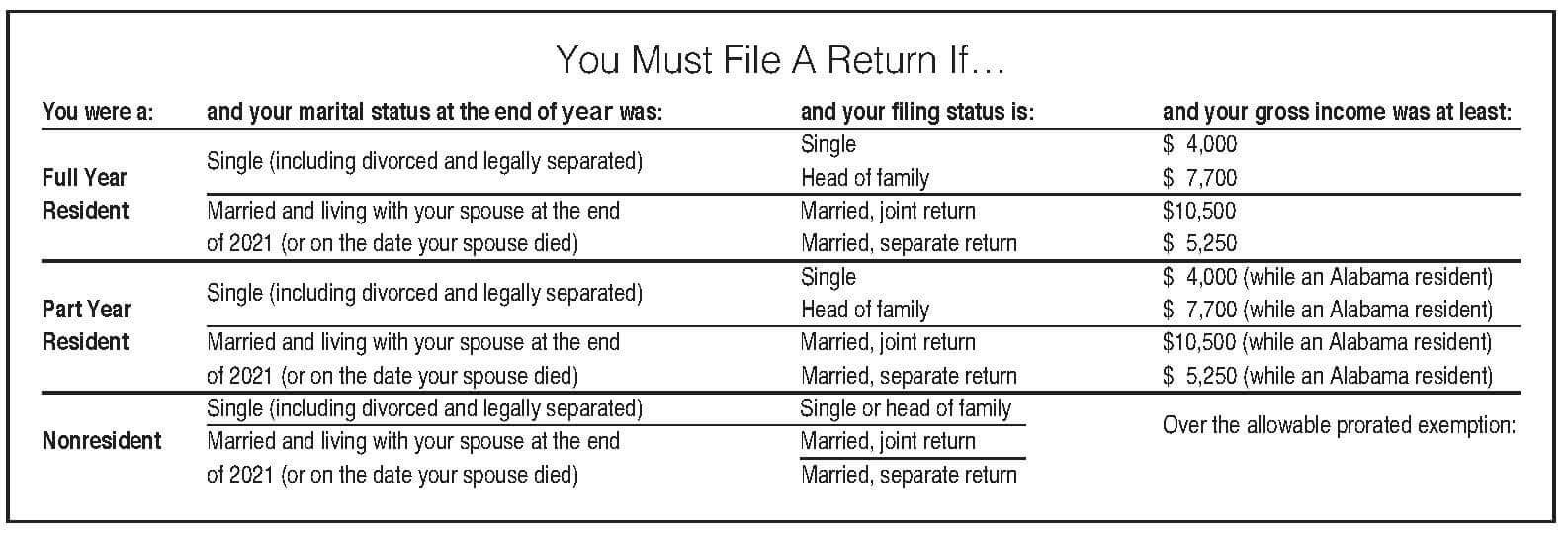

Filing Requirement:

Individuals who meet certain taxable income thresholds and are domiciled in Alabama are required to file an Alabama Individual income tax return.

Domicile – Individuals who are domiciled in (or residents of) Alabama are subject to tax on their entire income whether earned within or without Alabama. This is true regardless of their physical presence within Alabama at any time during the taxable year. Domicile is where one lives, has a permanent home, and has the intention of returning when absent. Domicile may be by birth, choice, or operation of law. Each person has one and only one domicile which, once established, continues until a new one is established coupled with the abandonment of the old. A temporary absence from Alabama does not automatically change your domicile for individual income tax purposes. Burden of proof regarding the change of domicile is on the taxpayer even though he/she owns no property, earns no income, and has no place of abode in Alabama.

Individual Income Tax Rate. Alabama has a graduated individual income tax, with rates ranging from 2% to 5% depending on taxable income and filing status.

For single, head of family, and married filing separate returns:

- 2% First $500 of taxable income

- 4% Next $2,500 of taxable income

- 5% All taxable income over $3,000

For married persons filing a joint return:

- 2% First $1,000 of taxable income

- 4% Next $5,000 of taxable income

- 5% All taxable income over $6,000

Filing Status and Personal Exemption:

There are four different filing statuses available under Alabama law:

Filing Status Personal Exemption

Single $1,500

Married Filing a Joint Return $3,000

Married Filing a Separate Return $1,500

Head of Family $3,000

For detailed description of each filing status visit Statuses for Individual Tax Returns.

When to File:

Original Due Date. The Individual income tax return is due on the same date as corresponding federal income returns are required to be filed, which is April 15 for most individuals. If the due date falls on a Saturday, Sunday, or state holiday, the return will be due the following business day.

Automatic Six-Month Extension to File: Individual Income Tax (Form 40, 40A, 40NR)

If you know you cannot file your return by the due date, you do not need to file for an extension. You will automatically be granted an extension until October 15. Except in cases where taxpayers are abroad, no extension will be granted for more than six months. Note: No paper or electronic extension form is needed to be filed to obtain the automatic extension.

An extension of time granted to file is not an extension of time for payment of the tax. If you anticipate that you will owe additional tax on your return you should submit your payment by the original due date of the return.

An extension means only that you will not be assessed a penalty for filing your return after the due date, however, interest and late payment penalty will be due on any additional tax due with the return from the due date of the return until the date of payment.

Which Form to Use:

FORM 40-A. Individuals may file a FORM 40A if you meet all the following conditions:

- You were a resident of Alabama for the entire year,

- You do not itemize your deductions,

- You do not claim any adjustments to income, such as IRA Deduction, alimony paid, federal income tax paid for a prior year, etc.,

- You do not have income from sources other than salaries and wages except for interest and dividend income which does not exceed $1,500.

FORM 40. You must use a FORM 40 if:

- You were a full or part-year resident of Alabama and do not meet ALL the requirements to file a FORM 40-A, and

- You are itemizing deductions.

Part-Year Residents

Part-year residents of Alabama should only report income earned while a resident of Alabama. Itemized deductions must be prorated to reflect only those expenses incurred while a resident of Alabama. Federal Tax Liability must be prorated by applying the same percentage of Alabama adjusted gross income to Federal adjusted gross income in order to calculate the amount deducted on line 12 of Form 40. Part-year residents are allowed to deduct the full standard deduction, personal exemption, and dependent exemptions.

FORM 40NR. You must use FORM 40NR if:

You are not a resident of Alabama and you received taxable income from Alabama sources or for performing services within Alabama and your gross income from Alabama sources exceeds the allowable prorated personal exemption or filing Married Filing Joint under the “Military Spouses Residency Relief Act.” Nonresidents must prorate the personal exemption. If your Alabama gross income exceeds the prorated amount, a return must be filed.

You must use both FORM 40 and FORM 40NR if:

You had sufficient income to require the filing of a part-year return and also had income from Alabama. Sources while a nonresident during the same tax year. In this case, both the total personal exemption and the dependent exemption must be claimed on the part-year resident return. No exemption can be claimed on the nonresident return. The part-year resident return should include only income and deductions during the period of residency, and the nonresident return should income only income and deductions during the period of non-residency.

Estimated Tax Payments:

If you owe additional tax for the previous year, you may have to pay estimated tax for the current year.

Taxpayers must make estimated income tax payments if their estimated Alabama income tax after credits and taxes withheld is expected to exceed $500. Calendar year taxpayers can pay the estimated tax in installments, on or before April 15, June 15, September 15, and January 15.

You can use the following general rule as a guide during the year to see if you will have enough withholding, or if you should increase your withholding or make estimated tax payments.

General Rule. In most cases, you must pay estimated tax for the current year if both of the following apply:

- You expect to owe at least $500 in tax for the current year, after subtracting withholding and credits.

- You expect your withholding plus your credits to be less than the smaller of:

- 90% of the tax to be shown on your current year tax return, or

- 100% of the tax shown on your previous year tax return. Your previous year tax return must cover all 12 months.

Refunds

If you do not receive your refund within 90 days of mailing your return, go to www.revenue.alabama.gov then click “Where’s My Refund” for an update. You can also call our 24-hour toll-free Refund Hotline at 1-855-894-7391.

Actions a taxpayer can take to have their refund processed faster:

- File electronically

- File your return early in the tax season

- Make sure your return is error-free

- Respond to letters from ALDOR

Common mistakes which delay a refund are:

- Incorrect name

- Incorrect address

- Incorrect Social Security number

- Return is illegible

- Missing W-2

- Incorrect computations

- Mailing return to the incorrect address

- Filing a copy of a return without the original signatures

- Missing signatures

Net Operating Loss (NOL) Provisions

Income Tax Incentives:

Alabama offers income tax incentives for individuals including incentives for new, existing, or expanding businesses in Alabama. For information on tax incentives available to business owners in Alabama, visit the Income Tax Incentives page.

See the Form 40 Instruction Booklet and the FAQs for information on income exempt from Alabama Income taxation other nonbusiness credits, deductions, and exemptions.

Consumers Use Tax

Use tax is the counterpart of the sales tax. State use tax is imposed at the same rate and on the same type of transactions as sales tax and is due from the consumer when the sales tax is not collected. When you purchase merchandise from a retail store or other business establishment in Alabama, the seller is required to collect sales tax on the purchase. When you purchase merchandise from a business located outside of Alabama the seller might collect sales or use tax on the purchase. However, not all out-of-state businesses are registered and required to collect Alabama tax. As the consumer, you are responsible for ensuring that sales or use tax is paid on your purchases. When you purchase merchandise for storage, use or consumption in Alabama and the retail seller does not collect tax on the purchase, you must report and pay consumer use tax on the purchase price. Consumer Use Tax can be reported annually on your individual income tax return.

ALDOR provides a spreadsheet, Consumers Use Tax Calculator, to keep track of all the purchases you made but did not pay sales tax on. This applies to retail purchases outside of Alabama, purchases from businesses on the internet, and the purchase of any retail items over the telephone.

Electronic Filing:

Alabama encourages taxpayers to file their Alabama income tax returns electronically. The benefits of e-filing your Alabama tax return include instant submission, acknowledgement or receipt and acceptance of filing, error checking, and faster refund response times. Most tax preparers can electronically file your return for you, or you can do it yourself for free through My Alabama Taxes or through paid income tax software.

For more information visit Individual Income Tax Electronic Filing Options.

Forms

To view a complete listing of forms for individuals, please visit the forms page. You may search by form number, title of the form, division, tax category, and/or year.

Most Popular Forms

- Form 40

- Form 40 Booklet

- Form 40-A

- Form 40-A Booklet

- Form 40NR

- Form 40NR Booklet

- From 40V Payment Voucher

Payment Information