Section 40-18-550 through Section 40-18-562, Code of Alabama 1975

The Rural Hospital Investment Program was created to help eligible rural hospitals across Alabama receive additional funding by providing a tax credit for qualifying donations.

The Rural Hospital Investment Program Board has been established to administer the Program. The Board is responsible for approving eligible rural hospitals for the program. Detailed information on the requirements to become an eligible rural hospital can be found below under “Additional Resources.”

Provisions of the Rural Hospital Investment Tax Credit include:

- The credit is available for each tax year beginning January 1, 2026, until December 31, 2028, unless extended by legislature.

- The credit may be applied against:

- Income taxes;

- Financial institution excise tax;

- Insurance premiums tax;

- Utility taxes paid; or

- 2.2% state utility license tax.

- Donors may receive a tax credit equal to 100 percent of qualified donations, subject to the following annual limits:

- Individuals filing single, head of household, or married filing separately: Up to $15,000.

- Individuals filing married filing jointly: Up to $30,000.

- Pass-through Entities: Up to $450,000.

- Corporations: The lesser of 100 percent of the donation or 75 percent of their income tax liability, up to $500,000.

- Financial Institutions: The lesser of 100 percent of the donation or 75 percent of their state excise tax liability, up to $500,000.

- Insurance Companies: The lesser of 100 percent of the donation or 75 percent of their insurance premium tax liability, up to $500,000.

- Utility Taxpayers: The lesser of 100 percent of the donation or the total utility taxes paid.

Note! To claim the credit against utility taxes, a taxpayer must have a utility tax direct pay permit. In accordance with Revenue Rule 810-6-5-.26.02, a utility tax direct pay permit is only available to a person or entity purchasing utility services and receiving more than one bill from any one utility company. - 2.2% Utility License Tax (utility companies): 100 percent of the donation, not to exceed the taxpayer’s tax liability.

- The credit is effective in the tax year in which the reservation is made.

- Any unused credit may be carried forward for up to three years but cannot be transferred to another taxpayer.

Additional Provisions Include:

- The tax credit has an annual statewide aggregate cap and an annual cap per eligible rural hospital.

- Statewide aggregate cap: $20 million for 2026, $25 million for 2027, and $30 million for all subsequent years.

- Cap per eligible rural hospital: $750,000 for 2026, $1,000,000 for 2027, and $1,250,000 for all subsequent years.

- Electing pass-through entities must report the credit on their Electing Pass-Through Entity return. Non-electing pass-through entities shall distribute the credit to their owners on a pro rata basis. Each owner receiving an allocated share of the credit may claim the credit up to the applicable filing limit based on the owner’s tax type.

- The Rural Hospital Investment Program Board has been established to oversee the development and operation of the Rural Hospital Investment Program.

- The Board is responsible for identifying eligible rural hospitals and ranking such hospitals in order of financial need. A list of eligible hospitals for the upcoming calendar year will be published on this page by December 1 each year. The list can be found under “Additional Resources” below.

- An Operations Manual detailing the eligibility and ranking process will be published annually. A copy of the manual can be found below under “Additional Resources.”

- Nonprofit organizations that wish to solicit, administer, or manage qualified donations for eligible rural hospitals must complete the Third Party Attestation Form for Eligibilityand submit a copy to the Board. The completed form should be submitted to incentives@revenue.alabama.gov no later than November 15, 2025.

- Third parties approved by the Board may accept donations on behalf of a donor wishing to make an unspecified donation. Such donations will be allocated to eligible rural hospitals that have not yet received the maximum amount of contributions based on the financial need ranking established by the Board.

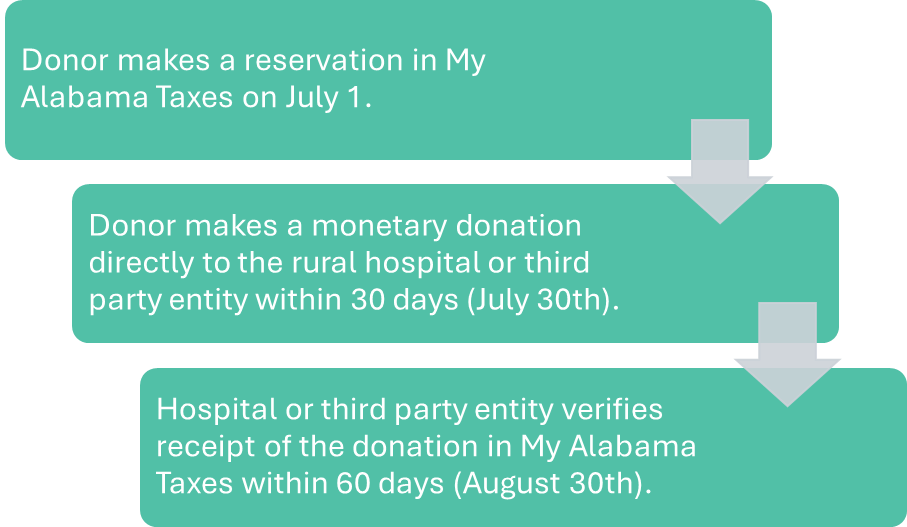

Credit Award Process

To be awarded the credit, eligible donors must first secure a credit reservation through My Alabama Taxes. After securing the reservation, a donor must make a qualifying donation and have the donation certified by an eligible rural hospital or third party within 60 days of the reservation date.

- For tax year 2026, reservations open January 5, 2026.

- Donors must reserve a tax credit through My Alabama Taxes. Reservations will be awarded on a first-come, first-served basis, subject to the applicable annual limits.

- When making a reservation, donors will specify an eligible rural hospital or third party to which the donation will be made.

- After making a reservation, donors have 30 days to make a monetary donation equal to the amount reserved to an eligible rural hospital or third party. A credit cannot exceed the reserved amount, even if the donation amount is greater than the reservation.

- Within 30 days of receiving the monetary donation, but no later than 60 days of the donor’s reservation date, the eligible rural hospital or third party must certify receipt of the donation through My Alabama Taxes.

Note! No credit will be awarded until the donation is received and certified by the eligible rural hospital or third party. If the donation is not made and certified within the required timeframe, the reservation will be forfeited.

Timeline Example:

*Any donations not verified by the 60th day of the reservation (August 30) are forfeited.