Section 40-9G-1 through Section 40-9G-2, Code of Alabama 1975

Under Chapter 9G of Title 40 (also known as the Alabama Reinvestment Act of 2015), certain reinvestment Under Chapter 9G of Title 40 (also known as the Alabama Reinvestment Act of 2015), certain reinvestment projects may qualify for sales, use and property tax abatements on capitalized replacement equipment and property purchased for capitalized repairs, rebuilds, renovations, and maintenance if the property is acquired as part of any addition, expansion, improvement, renovation, re-opening, or rehabilitation of a facility existing facility, or replacement of any existing equipment or tangible personal property that qualifies as a “qualifying project.” While this incentive can be used for facility expansion and equipment upgrades, Chapter 9G abatements are primarily for those companies undertaking projects such as reopening a closed facility, refurbishing an existing facility and/or purchasing replacement equipment.

Chapter 9G gives cities, counties, public industrial authorities, and the governor the authority to abate the following taxes:

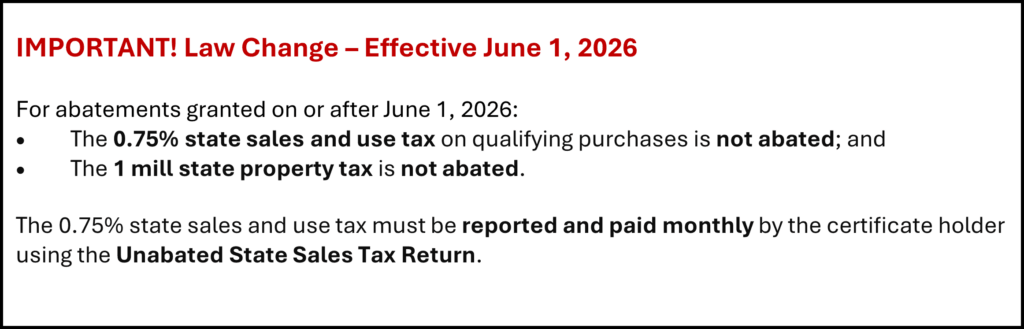

- State sales and use taxes except for the 0.75% unabated state portion;

- Non-educational county and city sales and use taxes;

- State property taxes, except for the 1 mill state property tax that remains unabated for up to 20 years.

- Non-educational county and city property taxes – up to 20 years.

To receive an abatement for any or all of these taxes, a project must meet certain qualifications and follow certain procedures, as determined by law and regulation.

Qualifying Project Requirements

- The project predominately involves an approved activity.

- You must invest at least $2 million in capital expenditures as part of any addition, expansion, improvement, renovation, re-opening, or rehabilitation of a facility, or replacement of any existing equipment or tangible personal property.

- No state project agreement has been or will be entered into with the governor for the provision of other incentives.

Chapter 9G Sales and Use Tax Abatements

Chapter 9G sales and use tax abatements are subject to and shall follow the same procedures, provisions, limitations, and definitions under Chapter 9B with two exceptions:

- Capitalized replacement equipment or tangible personal property can be abated under Chapter 9G; and

- Capitalized repairs, rebuilds, renovations, and maintenance can be abated under Chapter 9G.

The Chapter 9G sales and use tax abatements are granted by the same granting authorities under the Chapter 9B sales and use tax abatements.

Chapter 9G Property Tax Abatements

Chapter 9G property tax abatements are subject to and shall follow the same procedures, provisions, limitations, and definitions under Chapter 9B with a few exceptions:

- Capitalized replacement equipment and capitalized repairs, rebuilds, and maintenance on real and personal property can be abated.

- The amount of the property tax abatement shall be equal to the noneducational property taxes owed, minus the noneducational property taxes owed from the tax year immediately before the project was placed in service, specific to the property that is receiving an abatement.

- Regardless of the length of the abatement, the abatement may be granted as follows:

- City non-educational property taxes may be abated only with the consent by resolution of the governing body of the city.

- County non-educational property taxes may be abated only with the consent by resolution of the governing body of the county.

- State non-educational property taxes may be abated only with the consent of the governor.

- The governing body of a county and a municipality may separately authorize one or more public industrial authorities to provide by resolution for such consent on their behalf.

Additional Resources

- Act 2025-84

- Act 2026-550

- Act 2026-573

- Statutory Authority

- Approved Business Activity List

- Abatement Checklist

Chapter 9G Abatement Forms

Procedures for Alabama Reinvestment Act of 2015 Chapter 9G Abatements

To receive an abatement of sales and use taxes, property taxes, and/or mortgage recording taxes under Chapter 9G of Title 40, Code of Alabama 1975, certain actions must be taken by the private user, the granting authority, ALDOR, local taxing authorities, and/or the governor.General Overview of an Abatement Process

Private User

The private user is any individual, pass-through entity, or corporation organized for profit that is or will be treated as the owner of private use property for federal income tax purposes. Once a project site is determined, the private user must apply for the appropriate sales, use, and property tax abatements by submitting a completed “Application to Granting Authority for Abatement of Taxes” (Form CO:CAAG) to the appropriate governing body.

After the abatement is granted, the private user (or its representative) is responsible for submitting a completed abatement package to ALDOR within 90 days after the abatement is granted. The package must include the following:

- A copy of the executed abatement agreement;

- A copy of the certified resolution by the public body;

- A copy of the application to local granting authority (Form CO:CAAG) and the list of property to be acquired under the abatement;

- The certificate of exemption application (Form ST:EX-A2);

- Documentation that the private user is enrolled in the E-Verify program- https://www.e-verify.gov/;

- Proof that a copy of the resolution was submitted to the county commission must be sent to ALDOR if the abatement is granted by a municipality or a municipal industrial development board. The resolution must be either mailed by certified mail or by physical delivery to the county commission, and proof of delivery of affidavit or service (in the case of physical delivery), or by copy of certified mail receipt (in the case of mailing by certified mail), is required to be sent to ALDOR; and

- Project Notification with the Alabama Department of Commerce. You may contact the local Economic Development Agency for issuance of notification or please visit http://notification.madeinalabama.com/ to register your project online.

Once the completed abatement package is received by ALDOR, and if the abatement is for sales and use taxes, ALDOR will issue a certificate of exemption, which is used in making the necessary purchases to be incorporated into the project.

Note! Contractor(s) or subcontractor(s) who will be making purchases to be incorporated into the project must file an application for a certificate of exemption (Form ST: EX-A2) with ALDOR, along with a letter from the private user (or general contractor) verifying that they will be making purchases for the project.

For more information, visit Contractor Information:

Claiming the Sales and Use Tax Abatement

For projects granted a sales and use tax abatement, the state sales tax (excluding the 0.75% unabated portion) and the local sales and use taxes not earmarked for education are abated on qualifying tangible personal property incorporated into the project.

To utilize the abatement, all qualifying purchases must be made using a Sales and Use Tax Exemption Certificate for an Industrial or Research Enterprise Project. The certificate is issued to the private user (and, if applicable, its general contractor and subcontractors) and allows qualifying purchases to be made without payment of sales and use tax to the vendor.

The certificate holder is not required to file or remit state use tax on qualifying purchases. However, if the exemption certificate is used for items that do not qualify for the abatement, the applicable state and local taxes must be reported and paid.

The certificate holder is also required to:

- File and remit the Unabated State Sales Tax Return for the 0.75% state tax; and

- Remit any local sales and use taxes earmarked for education, either through ALDOR or directly with the local taxing authority, as applicable.

The certificate of exemption is effective as of the date the abatement is granted and expires upon completion of the project.

What is not included in the Sales and Use Tax Abatement for 9G Abatements

- Consumables or expensed items not subject to capitalization.

Claiming the Property Tax Abatement

For property tax purposes, the private user should contact the local county assessing official in the county where the property is located to claim the abatement for non-educational property taxes.

For the county assessing official to properly credit the abatement, certain information must be provided. The county assessing official must receive a copy of the abatement application, resolution, and abatement agreement. In addition, an itemized list of all abated property that has attained situs in Alabama as of October 1 and all of the existing property that is being refurbished/replaced must be provided before the abatement can be applied. Per Section 40-7-4, Code of Alabama, 1975, such property must be reported annually between October 1 and December 31 with the county assessing official. Therefore, property subject to abatement should be reported and identified as such each year on Form ADV-40, Business Personal Property Return (forms). Failure to provide this information to the local assessing official may delay the credit for the abated taxes.

Governing Body for Abatement of Taxes

The governing body is statutorily authorized to grant the tax abatements to qualifying projects and is subject to geographical or jurisdictional limitations.

Governing Body for Chapter 9G Tax Abatements for Sales and Use Tax

- A city may grant abatements (for certain state, county, and city taxes) to qualifying projects located within the city limits and police jurisdiction.

- If a city government abates county taxes, the city must notify the county by sending a copy of the abatement resolution to the county commission, by certified mail.

- If a city is the jurisdictional authority but does not abate the city’s corresponding taxes, the city must have consent from the governing body of the county by resolution to abate the county’s sales and use taxes.

- A county may grant abatements (for certain state, county, and city taxes) to qualifying located within the county, but not within the city limits or police jurisdiction unless consented to by resolution of the governing body of the municipality.

- A public industrial authority may grant abatements (for certain state, county, and city taxes) to qualifying projects located within the authority’s jurisdiction.

- If a municipal public authority abates county taxes, the municipal public authority must notify the county by sending a copy of the abatement resolution to the county commission, by certified mail.

- If a municipal public authority is the jurisdictional authority but does not abate the city’s corresponding taxes, the municipal public authority must have consent from the governing body of the county by resolution to abate the county’s sales and use taxes.

Governing Body for Chapter 9G Property Tax Abatements Granted for any or all Years 1-20

Each taxing jurisdiction must grant its own non-educational property taxes for abatements granted for any or all years 1-20 by adopting a resolution.

- A county may grant property tax abatements for any or all years 1-20 on property located in the county but only as to the county non-educational property taxes.

- A city may grant property tax abatements for any or all years 1-20 on property located within the limits of the city but only as to the city non-educational property taxes.

- The governor may grant property tax abatements for any or all years 1-20 on property located in the state but only as to the state non-educational property taxes.

- The governing body of a county and a city may separately authorize one or more public industrial authorities to provide by resolution for such consent on their behalf.

Responsibilities of the Governing Body

The governing body (county government, city government, and/or public industrial authority) must adopt a resolution granting the abatements for the applicable taxes. The abatements must be embodied in a written abatement agreement between the governing body (county government, city government, public industrial authority, and/or Governor) and the private user. The abatement agreement should specify the following:

- The private user(s) who is granted the abatement;

- An estimated amount of tax abated for each type of tax;

- The maximum exemption period for each abatement;

- Good faith projections, by the private user, of the amount to be invested, the number of individuals to be employed, and the payroll (initially and in the succeeding three years);

- 2012 North American Industrial Classification System (NAICS) code as provided to the private user by the Department of Labor or specific qualifying business activity allowed by statute; and

- If the project is for a reinvestment project (Chapter 9G) to an existing industrial development property, then the agreement should contain information to reflect that the addition is at least $2 million.

Limitations of Tax Abatements

An abatement applies to all real and personal property incorporated into the project. However, certain restrictions apply.

Sales and Use Tax

- For sales and use tax, the abatement becomes effective on the date the abatement is granted by resolution and continues to be in effect until the entire project is placed in service (with the exception of data processing centers). Only the purchases made after the abatement is granted will qualify for the tax abatement.

- Once the Certificate of Exemption is issued, it will be used to make all purchases of tangible personal property to be incorporated into the project, without incurring sales and use tax. If any purchases made with the exemption certificate do not qualify, the state and local sales or use tax will be required to be remitted.

- For sales tax, the overall capital purchases must not exceed the approved investment amount plus a 10% deminimis deviation. For the additional investment to be included, the abatement agreement must be amended to reflect the additional investment.

- ALDOR may review, audit, and conduct inspections and investigations of property for which abatements are granted.

Sales and Use Tax Filing and Payment Requirements:

- Certificate holders must file and remit the Unabated State Sales Tax Return for the 0.75% state tax;

- Certificate holders must also file a separate local tax return for any local sales and use taxes earmarked for education;

- State and local taxes must be reported and paid on any purchases that do not qualify for the abatement, even if the exemption certificate was used at the time of purchase; and

- If the project is located in a self-administered locality, the certificate holder is responsible for coordinating and remitting any local educational taxes directly with that local taxing authority.

Property Tax

- Once an abatement is granted, ALDOR will supervise the valuation, equalization, and assessment of the abated property.

- For property tax, if bonds are issued the abatement starts on the date the bonds are issued to finance the cost of the private use property; else, the abatement starts on the date the project is placed in service or such date as specified in the abatement agreement.

- An abatement for non-educational property taxes must not exceed 20 years from the date the abatement period begins (with the exception of data processing centers).

- No additional property (real or personal) may be eligible for abatement once the project is placed in service unless another abatement project is made.

- Once the maximum exemption period as defined by §40-9G-2 expires, all real and personal property will become fully taxable.

- A change of ownership or assignment of interest of an operating industrial or research enterprise does not qualify the property for a new or additional abatement. The new owner will be allowed to receive the remainder of abatements previously granted.

- For property tax, the overall real and personal property investment must not exceed the approved investment amount plus a 10% deminimis deviation. For the additional investment to be included, the abatement agreement must be amended to reflect the additional investment.

- The property tax abatement will terminate if the property ceases to be used in the active conduct of an industrial or research enterprise or the approved activity for six consecutive months.

- The amount of the property tax abatement cannot be calculated without the private user providing a listing of the existing property to be refurbished and/or replaced to the county assessing official. The amount of tax owed on the property being refurbished and/or replaced from the year immediately preceding the new property being placed in service will be the basis for the valuation calculation for the duration of the abatement.